The dealership is quiet. Too quiet.

You’re sitting across from a salesperson who has just asked a deceptively simple question:

“So… are you planning to lease or finance?”

You nod politely. Pretend you’re thinking. But inside your head, the real debate is happening:

Lease vs finance car, what’s actually the smarter move?

Because both options get you the keys. Both come with monthly payments. And both somehow sound like the “better deal” depending on who’s doing the talking.

Let’s slow it down. Strip away the sales pitch. And actually understand what you’re signing up for, before the paperwork slides across the table.

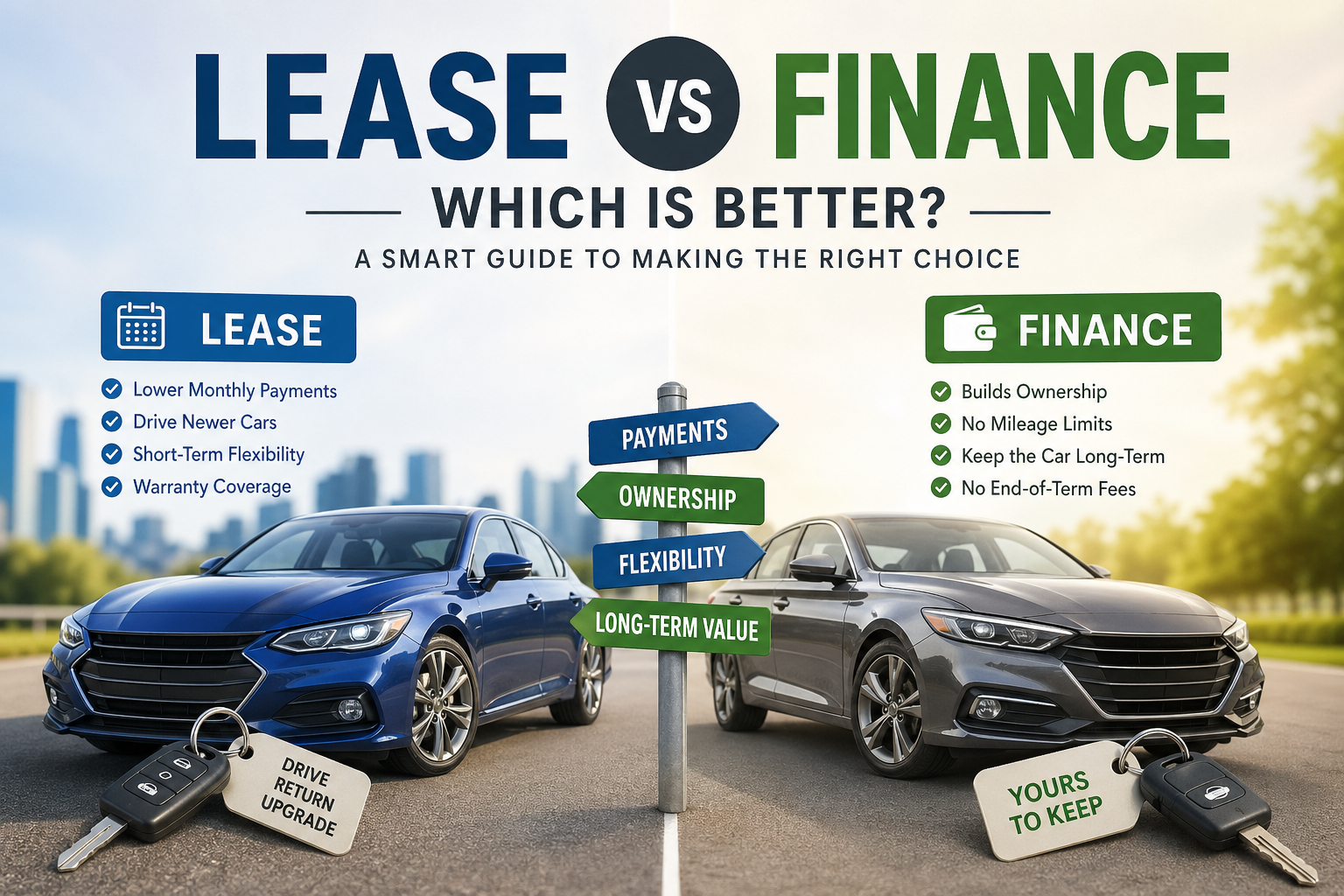

Leasing a Car: The Long-Term Test Drive

Leasing is often described as “renting a car,” but that’s a little too casual. It’s more like a structured, contract-heavy long-term test drive.

You’re not buying the car. You’re paying for the portion of its value that disappears while you use it, its depreciation.

Most leases run between 24 and 36 months. During that time, your monthly payments are usually lower than if you were financing the same vehicle.

That’s the hook. Lower payments. New car. Minimal commitment.

But here’s where it gets real: leases come with rules.

Typical lease agreements include:

- Mileage caps (often 10,000–15,000 miles per year)

- Strict wear-and-tear standards

- Fixed contract terms you can’t easily exit

Push past those limits, and the savings can quietly evaporate. Extra miles? That’ll cost you per mile. Scratches, dents, interior wear? Also billable.

According to the Federal Trade Commission, these end-of-lease charges are one of the most common surprises for drivers. You can read more in their guidance here.

So yes, leasing feels lighter month-to-month. But it’s not as flexible as it looks on the surface.

Financing a Car: The Ownership Route

Financing is more straightforward, and for many people, more emotionally satisfying.

You borrow money (usually through a bank, credit union, or dealership). Then you pay it back over time, with interest.

Typical loan terms range from 36 to 72 months.

At the end?

You own the car. Fully. No strings attached.

That changes everything.

No mileage limits. No return inspections. No “end-of-term” decisions.

Just a car that’s yours to drive, modify, sell, or keep until it barely starts on cold mornings.

The Consumer Financial Protection Bureau breaks down auto loans clearly here.

Of course, there’s a tradeoff. Monthly payments are usually higher than leasing.

Because you’re not just paying for depreciation, you’re paying for the entire vehicle.

Lease vs Finance Car: Where the Differences Actually Matter

On paper, the distinction seems simple. But in practice, the choice affects your finances, your flexibility, and even how you think about driving.

Let’s break it down where it counts.

1. Monthly Payments

Leasing usually wins this round.

Since you’re only covering depreciation, your monthly payment is typically lower than financing the same car.

That’s why leases can make more expensive vehicles feel accessible.

Financing? Higher payments, but every dollar builds ownership.

Short-term relief vs long-term payoff.

2. Ownership (Or Lack of It)

This is the philosophical divide.

Financing means eventual ownership. Leasing means perpetual borrowing.

At the end of a lease, you have three options:

- Return the car

- Start a new lease

- Buy the car (usually at a pre-set price)

With financing, there’s no decision at the end. The car is already yours.

And that matters more than people expect.

Because once the loan is paid off, your monthly car expense drops to… zero.

Leasing never gets you there.

3. Mileage Freedom

If you drive a lot, this is where leasing can quietly punish you.

Lease contracts limit your annual mileage. Go over, and you’ll pay for every extra mile.

Financing doesn’t care how far you drive.

Road trips, long commutes, spontaneous weekend drives, none of it comes with penalties.

If your lifestyle involves movement, financing gives you breathing room.

4. Maintenance and Repairs

Leasing has one subtle advantage: predictability.

Since leases are short-term, most vehicles stay under warranty the entire time. That means fewer surprise repair bills.

Financing? It depends how long you keep the car.

Once warranties expire, maintenance becomes your responsibility.

That said, many drivers are happy to accept that tradeoff, especially if it means avoiding endless payments.

5. Driving the Latest Model

Leasing is built for people who like change.

Every few years, you get a new car. New tech. Better fuel efficiency. Updated safety features.

It’s a cycle: lease, return, upgrade.

Financing is different. You’re more likely to keep the car longer, especially once it’s paid off.

For some, that’s stability.

For others, it feels like being stuck with outdated features.

When Leasing Actually Makes Sense

Leasing isn’t a bad deal. It’s just a specific deal.

It tends to work best if you:

- Prefer lower monthly payments

- Enjoy driving newer cars regularly

- Don’t drive excessive miles

- Want fewer maintenance worries

- Value convenience over ownership

There’s also a psychological angle. Leasing keeps things simple.

No long-term commitment. No resale concerns. No thinking about depreciation years down the line.

Just drive, return, repeat.

When Financing Is the Better Move

Financing shines when you’re thinking beyond the next two or three years.

It usually makes more sense if you:

- Plan to keep your car long-term

- Drive a lot annually

- Want full control over your vehicle

- Prefer to eliminate monthly payments eventually

- See a car as an asset, not just a utility

Because here’s the quiet truth about financing:

The best part isn’t owning the car.

It’s the moment you stop paying for it.

The Hidden Costs People Forget

Here’s where things get interesting, and often overlooked.

Leasing Hidden Costs

- Excess mileage fees

- Wear-and-tear penalties

- Early termination fees

- Continuous monthly payments (if you keep leasing)

Financing Hidden Costs

- Interest over time

- Maintenance after warranty expires

- Depreciation (especially in early years)

Neither option is “cheap.” They just spread costs differently.

Leasing compresses expenses into a shorter, predictable window.

Financing stretches them out, but gives you something permanent at the end.

So… Lease vs Finance Car: Which Is Better?

There isn’t a universal answer. And that’s not a cop-out, it’s the point.

Leasing is about flexibility, lower upfront cost, and staying current.

Financing is about ownership, long-term savings, and independence.

If you like change, predictability, and lower payments → leasing will feel comfortable.

If you like control, long-term value, and eventually paying nothing → financing will feel smarter.

The real question isn’t just financial.

It’s behavioral.

Do you want to keep upgrading… or eventually be done paying?

Frequently Asked Questions (FAQs)

Is leasing always cheaper than financing?

Not necessarily. Leasing has lower monthly payments, but since you never own the car, you may spend more over time if you keep leasing repeatedly.

Can you negotiate a lease?

Yes. Many aspects, like the car’s price, mileage allowance, and fees, can be negotiated, even if it doesn’t feel obvious.

What happens if I want to end a lease early?

Ending a lease early can be expensive. Most contracts include early termination fees, which can offset any savings.

Is financing better for long-term savings?

Generally, yes. Once your loan is paid off, you can drive payment-free, which leasing never offers.

Can I buy my leased car?

Often, yes. Most leases include a buyout option at the end of the term, based on the car’s residual value.

The next time you’re in that dealership chair, the question will come again:

“Lease or finance?”

This time, you won’t just nod.

You’ll know exactly what you’re choosing, and why.

*This article is for informational purposes only and should not be taken as official legal advice*